MYR Group currently trades at $124.23 and has been a dream stock for shareholders. It’s returned 506% since March 2020, more than tripling the S&P 500’s 152% gain. The company has also beaten the index over the past six months as its stock price is up 24.4% thanks to its solid quarterly results.

Is there a buying opportunity in MYR Group, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Despite the momentum, we're cautious about MYR Group. Here are three reasons why we avoid MYRG and a stock we'd rather own.

Why Do We Think MYR Group Will Underperform?

Constructing electrical and phone lines in the American Midwest dating back to the 1890s, MYR Group (NASDAQ:MYRG) is a specialty contractor in the electrical construction industry.

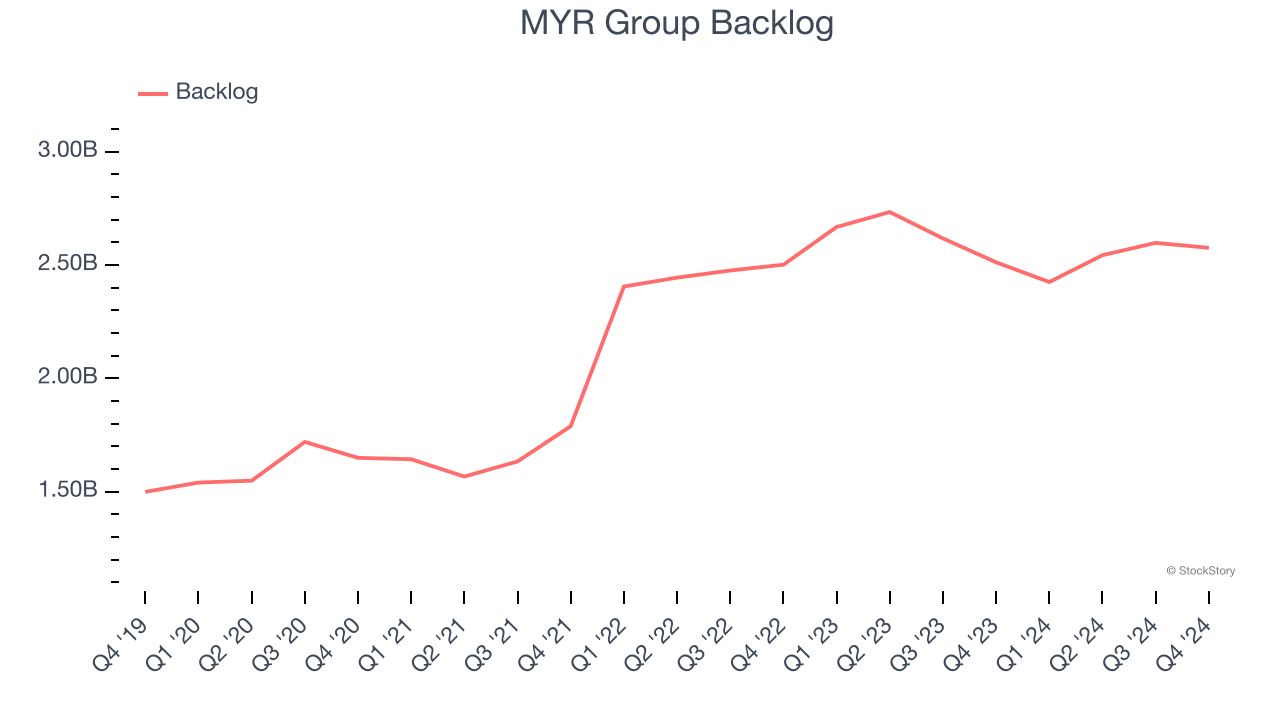

1. Weak Backlog Growth Points to Soft Demand

Investors interested in Construction and Maintenance Services companies should track backlog in addition to reported revenue. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into MYR Group’s future revenue streams.

MYR Group’s backlog came in at $2.58 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 1.8%. This performance was underwhelming and suggests that increasing competition is causing challenges in winning new orders.

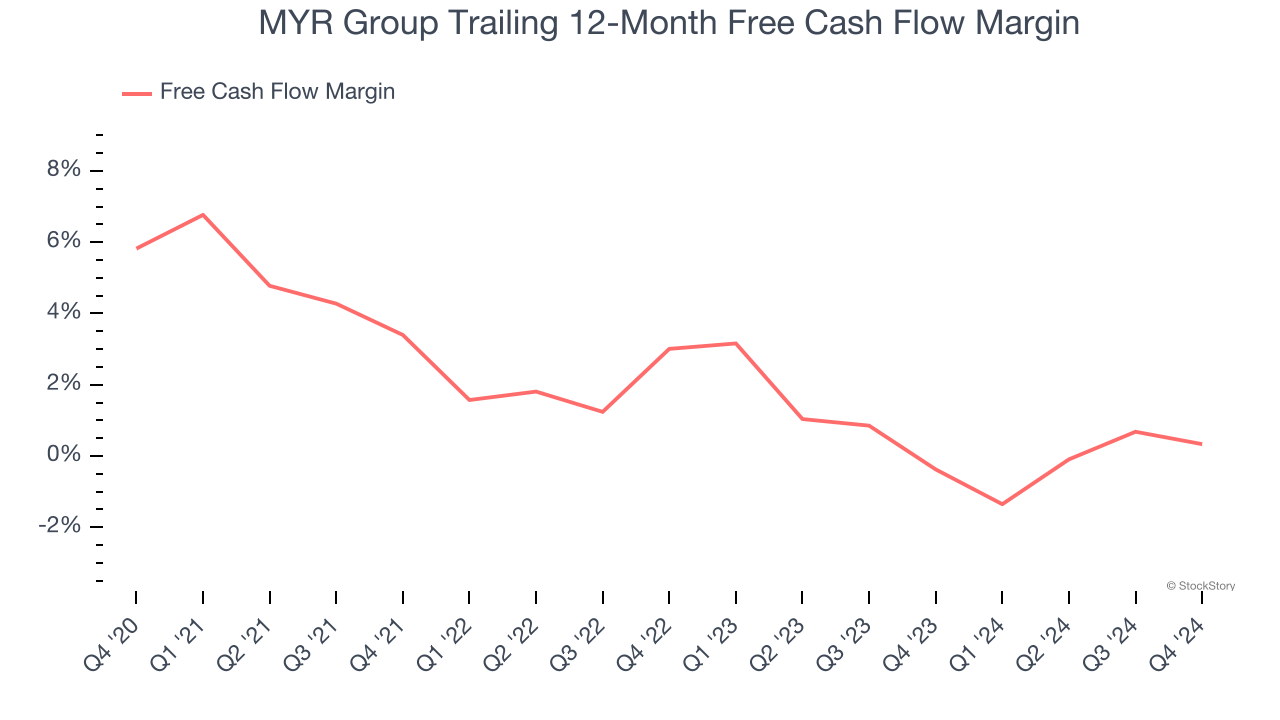

2. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, MYR Group’s margin dropped by 5.5 percentage points over the last five years. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s becoming a more capital-intensive business. MYR Group’s free cash flow margin for the trailing 12 months was breakeven.

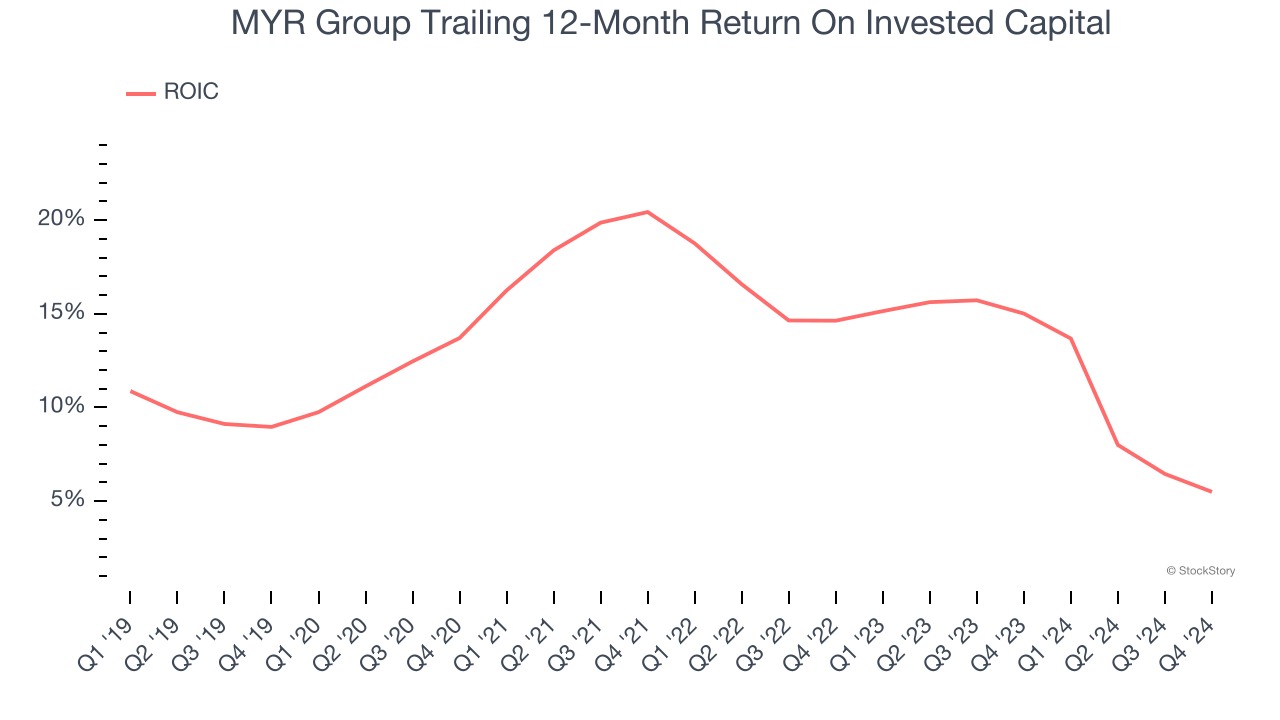

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, MYR Group’s ROIC has decreased over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

MYR Group falls short of our quality standards. With its shares topping the market in recent months, the stock trades at 21.4× forward price-to-earnings (or $124.23 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. We’d recommend looking at the most entrenched endpoint security platform on the market.

Stocks We Like More Than MYR Group

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.